This piece was jointly written with a working group on inflation of Groups against Capital and Nation.

Version: 2023-02-05

In this piece, we aim to explain what inflation is. To do that, we need to explain credit, credit money and sovereign debt. As a consequence, this piece has gotten rather long. We start by criticising popular explanations of inflation as given by central bankers and financial journalists. This section concludes by formulating the question that we aim to answer in the remainder of this piece: how is it that the participants of a capitalist economy devalue the very thing around which their activities revolve: money? The answer has two parts. In Section 2 we explain how inflation of, say, 2%, 5%, 10% is a by-product of successful capitalist accumulation. In Section 3 we explain how runaway or hyperinflation is a product of the State’s reaction to an economic crisis. That is, the different quantitative rates of inflation correspond to qualitatively different causes.

The Question

The financial press and (monetary) policymakers offer up a variety of causes for inflation: from labour shortages and supply chain disruptions to a “persistence of demand for goods”, “higher global prices for goods”, energy prices and war, see “Press”. These are rather questionable explanations.

No subjects, anywhere.

The starting point of debates about high inflation in the financial press or by monetary policymakers is that “we” are all affected by inflation. Inflation is not something some subjects in the economy produce through their actions but something that happens to everyone. Inflation is something that happens to which we (mostly the Central Bank) then react. Yet, like anything else in the economy, this result is not produced by anyone but the market participants. What appears to these commentators like a mysterious natural law affecting our economies is the joint product of those who experience it.1

The refusal to grasp inflation as the product of economic actors goes as far as ignoring those who increase prices. “Strong demand for most goods and services” (FT 18 Jan 2022) only adds inflationary pressure if the sellers increase prices and profit from this increased demand. At the very least such an “explanation” of inflation would need to address that someone’s bottom-line calculation makes them exploit the increased effective demand for their commodities; (even leaving aside the pressing question, for now, where the purchasing power of this increased effective demand comes from).

Victims, everywhere.

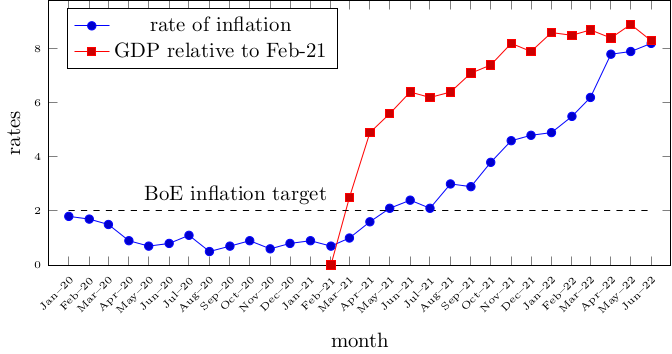

There is a second way in which – according to commentators in the press – we are all affected by inflation. The consensus is that inflation (above 2%) is bad for an economy and its participants.2 Yet, for those starting the process by increasing prices and profits in response to strong demand, i.e. those who are not yet confronted with increased prices by their suppliers, for those inflation at least initially pays off. Also, for those who can turn their increased costs into increased prices, where is the problem?3 Their profit rate is unaffected. When inflation started rising in 2021 this happened in a period of strong economic growth (FT 30 Jul 21, 12 Aug 21), cf. plot. This was not a situation where fewer commodities were bought and sold because their prices increased – higher prices were paid without a collapse in the volume of sales.

Of course, many people do not have the freedom to adjust the price of what they are selling if their costs increase. The plight of workers, whose wages or benefits do not scale with inflation, is discussed under the heading of the “cost of living crisis”. Now, one could be forgiven for thinking that the Bank of England’s worry must be that workers’ livelihoods are left behind as inflation soars. Yet, the opposite is true and the BoE keeps warning of a wage-price spiral where – ostensibly, see below – higher wages trigger further inflation and thus are best avoided (FT 5 Aug 21, 1 Feb 22). We would have to ask why that would be so bad. If everyone had more money then increased prices would not hurt anyone, people would still be selling, say, 8 hours a day to be able to rent, pay bills and groceries regardless of whether 8 hours of their labour time are represented by £80 or £800. The BoE’s worry must come from elsewhere.

Higher wages do not produce inflation.

Also, the claimed relationship between wages and prices is false. Say, Alice hires Bob to make widgets for her. She pays him £10 per widget, each widget also requires £10 worth of raw materials and tools and Alice manages to sell those widgets for £30. After paying Bob and for raw materials, Alice is left with £10 to turn into cigars for her personal consumption. Now, assume Bob manages to convince Alice to pay him £15. Unless something else changes, Bob now goes home with £15 per widget and Alice with only £5. The key point here is that whatever purchasing power Bob gains, Alice loses and vice versa. We witness a redistribution of wealth, Bob can now afford some of the commodities previously enjoyed by Alice, who is now priced out of these commodities. So, for example, the cigars previously enjoyed by Alice may now partially be enjoyed by Bob.

Of course, Alice may try to increase the price of her widgets to £35 to recover her previous profits of £10 per widget. Yet, if Alice has the freedom to set the price of her widgets according to her personal profit appetite why did she not set it to £50, £100 or £200 to begin with? If employers could simply come up with prices that match their profit preferences they would not have to keep wages (and other costs) down. Put differently, employers in 2022 were not enduring a hot summer of strike action because they heed the BoE’s warning that increased wages might lead to inflation, but to protect their bottom line. That is to say if Alice manages to increase the price per widget without shrinking the volume of widgets she sells (this shrinkage would harm Alice’s aim of recovering her previous profits) then additional ability to pay must confront her.

Thus, we must consider not only Alice and Bob but the case where (essentially) all workers in society receive a pay rise.

Then, if, on the one hand, “widget” in the example above stands for commodities that are purchased by both workers and employers (either as employers or as private persons enjoying the spoils of their business) then the Alices of this world – i.e. the employers – are confronted with a market situation where part of their clientele has more money (workers) and another part has less (other employers). Now, remember that Alice’s attempted price increase is her reaction to reduced profits and here we assume that is a situation faced by essentially all employers because it affects essentially all workers. Alice and her competitors can sell more to workers but sell less to fellow employers; ability-to-pay in total did not increase by the same argument as above: an increase in wages is a reduction in profits and vice versa.

If, on the other hand, “widget” in the example above stands for commodities that are only purchased by workers then Alice’s customers indeed have more money to spend. Thus, Alice could indeed be successful in her endeavour to increase prices. Yet, the flip side still is that other employers have less. Thus, the market for, say, tinned beans improves whereas the market for cigars and sports cars is in trouble. Alice, who per our assumption in this paragraph is in the business of making tinned beans, makes a tidy profit, but her fellow employers producing cigars do not. By the same logic as applied to inflation, prices for cigars would drop. In response, other employers will switch their production to tinned beans instead of cigars which pushes down the price of tinned beans.

Single commodities becoming more expensive does not produce inflation.

That is, it would not even imply inflation if Alice and her competitors were successful in establishing a higher price for widgets. If the price of widgets increases that means, all else being equal, less spending power on other commodities. If people have £100 to spend and now spend £35 instead of £30 on widgets, they only have £65 instead of £70 left over.

All commodities becoming more expensive is not inflation as we know it.

Now, say the price of energy rises, a commodity that goes into the production of (pretty much) every other commodity, which makes (pretty much) all commodities more expensive. Yet, if this is not matched by an increase in purchasing power this simply means fewer commodities are sold. But, as mentioned above, this is not the phenomenon that (fully) corresponds to the current inflation. When inflation got going in Spring 2021 economies were reopening, COVID-19 restrictions were lifted and economies were growing, cf. plot.4 This again provokes the question of where the additional purchasing power came and comes from to realise these increased commodity prices in the same if not increased volume.

A description is not an explanation.

What many of these “causes” have in common is that they, in actuality, do not attempt to explain inflation but merely to describe it. When they come in the form of an explanation they offer a mere tautology. This is most explicitly expressed by the cause “higher global prices for goods” (FT 1 Feb 22) which tautologically explains price increases with price increases. The reason why the editors of financial journalists do not instruct them to revise and resubmit when confronted with such a logical fallacy is that to them inflation is simply what it is measured as. In e.g. the Consumer Price Index (CPI), inflation is measured in a basket of goods, how many Pound Sterling are required to purchase a defined collection of commodities. If that number goes up, we have inflation. Now, to explain why this number goes up they can point to energy, “clothing and footwear” (FT 16 Feb 22) or the prices of all goods. They are simply saying “the weighted sum of these prices went up because this part of the sum went up”. In other words, they are describing their sums but they are not explaining inflation, i.e. they are not explaining the economic phenomenon that makes prices in society rise.

Inflation is money losing value compared with itself.

The price of a commodity is an expression of its value in money. It is a ratio of the value of the commodity to the value of money. This ratio can go up – prices increase – (a) when the value of commodities increases or (b) when the value of money goes down.

-

The case (a), commodities becoming more valuable, boils down to explaining how prices of commodities are formed, which means explaining the substance of what is expressed in a price – value – and how prices are established on the market through supply and demand. Marx gives the fundamentals of the laws covering the values of commodities in Chapters 1 and 3 of Capital, Vol. 1. He discusses the necessary persistent divergence of prices from values in Chapter 9 and supply and demand in Chapter 10 of Capital, Vol. 3. However, as mentioned above, a theory of inflation would need to explain not only the shifts in value but also where the additional purchasing power is coming from as prices rise; commodities “simply” becoming more valuable does not.

-

The case (b) is money losing value compared with itself. Here, what appears in the prices of commodities is caused by a change in the value of money. As an analogy consider the weight of cats. A kitty, Fluffy, may gain or lose weight and the reasons for this are fairly well understood. It is an entirely different thing and a much more challenging riddle if “1 kilogram” changes its meaning, i.e. if kilogram per Fluffy changes because “the kilogram” changes. So, here, somehow in their economic activities, the subjects of a market economy devalue the very thing around which their activities revolve: money. How that works is the open question under the heading “inflation”. As we shall see below, explaining how money loses value compared with itself also delivers an explanation for the presence of additional ability to pay realising the increased commodity prices.

In other words, money losing value is – we claim – what inflation is in a strict sense. An indication that this is the case can be found in that the institutions tasked with managing and controlling inflation – the Bank of England and other central banks – are the institutions in charge of society’s money. They do not attempt to tweak prices (say, by building more nuclear power plants to reduce the impact of the price of oil on other commodities) but rather adjust the interest rate to control inflation.

PS: Inflation ≠ currency exchange rates.

Before we dive in, a word of caution. Inflation is a phenomenon separate from currency exchange rates. If the Pound loses against the Euro then this is not the same as the Pound losing value compared to its past self. If both the Euro and the Pound face 2% inflation, this can leave their exchange rate unchanged, or it may change for other reasons. Vice versa the exchange rate can remain constant even under different rates of inflation.

Inflation I: A Side-effect of Capitalist Accumulation

The question we arrived at in the last section was: How is it that the economic activities of the participants in a capitalist economy undermine the value of the money they do business in?

The Bank of England’s practical answer to this question is “supply and demand” for money:5

“The Bank of England has the job of setting monetary policy – the set of tools used to keep inflation low and stable. The main way we do that is through interest rates. An interest rate is the amount of money people get on any savings they have. It’s also the charge they need to pay on their loans and mortgages. So what’s the link between the interest rates and inflation? Higher interest rates make it more expensive for people to borrow money and encourage them to save. That means that overall, they will tend to spend less. If people on the whole spend less on goods and services, prices will tend to rise more slowly. That lowers the rate of inflation.” — Bank of England. What is inflation? 3 Feb 2022

“to borrow money”

Let us consider the existence of these “people”. The spending power available to most people does not derive from cheap credit, but from them selling something, typically their time to an employer. They must sell their ability to work to a business because they have necessities to pay for: rent, groceries, data plans, etc. For them to be a buyer requires them to have been a seller before.6

“encourage them to save”

A “cost of living crisis” is in public discourse because these necessities are, well, rather necessary. The question whether to save more or less is not on people’s minds but how to make ends meet. Faced with these problems it is rather fanciful to suggest that their choice to cash in on higher interest rates – a decision made by people dependent on wages and advised by the BoE to swallow a restriction in their living standards – is what brings down prices.7 The Bank of England can buddy up all it wants, what it describes here is not “people”.

Instead, the Bank means businesses.8 But then the explanation needs to account for the fact that, apparently, the ability to pay of businesses comes about differently than that of most people. Businesses are not constrained in spending what they have earned but spend, routinely and on a large scale, with borrowed money. Yet, the Bank does not even deal with businesses directly but with private banks.

“The main way we do that is through interest rates. An interest rate is the amount of money people get on any savings they have.”

The word “an” does a lot of work here. That is, a problem with this intuitive explanation is that the Bank does not set the interest rates that people are charged or paid.9 These are set by financial institutions according to their private calculations based on their mutual competition and the general development of business. The Bank of England sets the interest rates that financial institutions pay when borrowing from (and receive when lending to) the Bank of England. This usually does affect the interest rates charged by private banks but to the BoE’s frustration since 2013 this relationship is anything but direct.10 So an explanation would also have to account for how a capitalist economy relies on continuous credit from the Central Bank to private banks.

This means that somehow – according to the Bank of England – the interest rate it charges and pays to private banks and the private credit operations of these banks with businesses affect the stability and value of the money that the Bank of England issues. Note that when businesses take their loans and invest, they produce commodities, i.e. the things they and their workers buy with money. So, here, both sides come together: the ability to pay that is not backed by previously earned income but backed instead by credit and also additional commodities being produced. Somehow, this process is presently proceeding in a way that undermines – to an extent that worries the Bank of England – the very thing that measures its success, i.e. measures profit. So let us start there then: profit making.11

Credit creates growth

Prices are what businesses calculate with.

Capitalist enterprises invest money to make a return. They buy raw materials and machines and hire workers, put these to work and (aim to) sell the result for money.

For this to work out, companies need to find on the market sellers of the “inputs” they need – for the right price – and purchasers of the “outputs” they produce – for the right price.12

This means, first, that to earn money in a sale, some other party must have acquired money beforehand to now be able to pay. The success of other businesses is the premise for the success of individual businesses. This is analogous to the everyday experience described above.

This means, second, that in the acts of exchange, sales and purchases, the prices of goods and thus the values of money and commodities are presupposed. For example, the price of timber enters the calculation for a company deciding if they should buy it to put it to profitable use.

Money is the standard of success.

Third, through the prices on the market, businesses find out if they are successful, i.e. the sum of prices of raw materials, machines and labour time on the one hand and the prices their product fetches on the market on the other hand.

Capitalist success is measured by the difference between (the sum of prices of the) investment and (the sum of prices that make up the) return: profit. To decide whether a company did well or poorly in the last quarter, the standard is the surplus, counted in money. That is, the standard by which capitalist enterprises judge their own performance presupposes a value of money. Their calculations start and end with money, the unit with which they calculate and do not question.13

Money is the ultimate means of success.

Now, to produce this success they measure in money, the necessary and – on average – sufficient condition for success is having money in sufficient quantity. All means of competition can be purchased, for a price. Workers can be hired, as can managers to squeeze them, raw materials, better machines, transport deals and advertising. Of course, investments still can and do go bad, but everything that is needed to succeed is available for a price.

Credit is premised on capitalist growth.

Under these conditions, where a sum of money promises to turn into more wealth over time because money is the only thing needed to make this happen, money itself receives a price: “interest”. This is the price for the utility of money to be turned into more, the price for the useful quality of money to make profits.14

There is a fundamental difference between credit taken by businesses to run and expand their business and the sort of credit payday lenders offer. The former interest charge partakes in the success of capitalist enterprises, the latter squeezes the already insufficient income of the borrower. The former allows the debtor to grow their income which allows them to repay the loan with interest, the latter takes from the limited income of the debtor. The former partakes in the enrichment of the debtor, the latter impoverishes them.15

This partaking in the enrichment of the debtor is the basis of the modern banking system which collects all money in society that is lying idle at the moment – i.e. they borrow it and promise interest as a lure – and makes that the foundation for its lending business against higher interest rates.

Credit is the foundation of capitalist growth.

This allows businesses to turn their growth and their competitive behaviour upside down. They no longer simply advance their own money, reap the profits and turn those into bigger advances for even bigger profits. Rather, they borrow money against interest, expand their business with this loan, pay the interest with a part of the profit then made and pocket the other part themselves.

Capital growth is not constrained by the profits already made, but only by the business outlook, how promising they are as debtors to those willing and able to extend credit. This alters the calculation for businesses in that profits are no longer the basis for growth. Rather, debt is the basis for this growth and profits must justify the creditworthiness to acquire debt.

In a developed capitalist society, this is not a one-off process, along the lines of: a company takes out a loan, makes an extension that works and then the loan is repaid with interest. Afterwards, the company has grown and returns to operating using only its profits. Rather, credit remains a permanent instrument of capitalist growth for businesses (and indeed the central means to start businesses, too). If the cycle – debt, business, debt has been justified – works then this is the best argument for both lenders and borrowers to continue the same on a larger scale. Growth anticipation attracts credit.

Growth anticipation creates credit

Above we wrote “the modern banking system […] collects all money in society and makes that the foundation for its lending business against higher interest rates”. The word “foundation” carries a lot of meaning here, which we unpack next. In summary, banks do not simply redistribute money in society and charge a fee for this service but they create ability to pay through their credit operations.16

Credit replaces money until it is paid off.

The simplest, spontaneous, form of credit is commercial credit, a form of credit that does not even involve financial institutions. Here, traders grant each other late payments of the form: “We have a regular business arrangement, I will take hold of the stock you delivered to me and will pay you in a week when my payments came in.” Here, the promise of future payment by a solid business temporarily replaces the payment in actual money (until the debt is settled). The promise of future payment generates the ability to pay that temporarily displaces money.17

Promises to pay become means of payment.

The next logical step is that debts circulate. Alice wrote a promissory note, “note payable” or “bill of exchange” to Bob: I will pay you £10 in one week.18 Now, Bob has to pay Charley. If Charley accepts the promise to pay by Alice then Bob can pay Charley with the promissory note issued by Alice. Bob hands over the note to Charley. Alice now owes the latter rather than Bob. Bob settled his sale to Alice and his purchase from Charley without involving actual money.19 The displacement of money by bills of exchange now goes beyond Alice and Bob but in the end Alice has to settle the debt in money.

Promises to pay replace and not just displace payment in money.

Next, debts are settled with debts. Say, Charley also needs to pay Alice, i.e. we have a circle: Alice needs to pay Bob, Bob needs to pay Charley, Charley needs to pay Alice. Then Charley can just use the promissory note from Alice to cancel out the payments, along the lines of “you owe me £5, I owe you £10, so I will pay you £5 and the matter is settled”. Of course, such a neat cycle is unlikely but in clearing houses a large number of such notes can be and were looked at together to cancel out debts where possible and to settle the difference.20

Here, promises to pay replace and do not simply anticipate or displace actual payments in money. The ability to pay, effective demand, is created without ever involving money. Promissory notes circulate in one direction but no money (to settle the debt) circulates back (later). This means that promises of payment create ability to pay separate from actual money, an ability that might not otherwise exist.

However, in the example above, if Charley does not cough up £5 to give to Alice then the foundation of the entire cycle is threatened. The foundation being to equate promises of future payment in £10 with the ability to pay or with “as good as paid”. If that equation is invalidated then the whole construction of using promissory notes in place of money may collapse. So here promises to pay replace money except that the differences to be settled have to be settled in hard cash, otherwise the whole system may come crashing down.

Banks organise commercial credit for their loan business.

All of this depends on Charley’s verdict about Alice’s ability to pay when payment from Bob is demanded. Charley will only accept a promissory note by Alice if he believes in the validity of this promise. In the olden times (until roughly 1900), banknotes were a way for banks to inject themselves into this relationship. Their offer was: bring your promissory notes to me and I will replace them with my promissory notes – “banknotes” – that are, however, at any point redeemable into real cash.21 You can then circulate these banknotes instead of real cash to go about your business. When this works then these banknotes increase the ability to pay in society purely on the basis that society believes these banks can live up to their promise to exchange them for real money; back then that was gold.

An approximate modern analogy is a bank account and bank transfers. The former is essentially a promise of payment on demand from the bank and the latter transfers such promises. When Alice brings £100 to her bank Barclays, the bank credits £100 to Alice’s bank account. When Alice now needs to pay, say, £10 to Charley, who happens to also bank with Barclays, then she can simply instruct Barclays to subtract “10” from her account and add “10” to Charley’s. No real money needs to be moved for this transaction. When Charley banks with Deutsche Bank then Barclays and Deutsche Bank engage in a similar process as described above: In total, today £1000 was paid from your customers to mine and £900 from my customers to yours, so you pay me £100 in real money and that’s that. In this example, £100 in money sufficed for exchanges totalling £1900.

Where this bank account analogy breaks down is that while the economic activity affected by this money is significantly greater in monetary value than the sum of money involved, in the examples so far no new purchasing power was created. When Alice deposited £100 into her bank account the bank took possession of her £100 in real money. The bank owes £100 to Alice and holds on to £100 in cash. The example so far is as if a bank account was simply a reference to a hoard of money in the bank’s vault.

A more complete modern analogy is getting a loan from a bank. When Eve gets a loan from Barclays the bank credits, say, £100 to her account. In return, Eve owes the bank £100 plus interest at some later point. She may have had to deposit a title to her house, some promise to pay by some business or some other security to secure the loan. Now, Eve can dispose over the £100 in her bank account in the same way as Alice could before. Movements within Barclays are just updates to the ledgers there, money movements between banks are settled by transferring only the difference (at the end of the day).

Liquidity management.

It is here where Barclays needs to be careful. If Eve pays £100 to Charley at Deutsche Bank and no Deutsche Bank customer sent money the other way then Barclays better have those £100 lying around in hard cash to pay out Deutsche Bank. If £90 are coming in from Deutsche Bank then £10 in hard cash are sufficient to settle the difference.

Anticipating these required amounts of hard cash and having them on hand when needed is called “liquidity management” by financial capitalists. Different strategies exist for managing it. Having cash at hand is one. Holding on to well-trusted promissory notes (say, issued by a well-known company or by the State, see below) that can be sold quickly if needed is another. Borrowing the money that is needed to pay off Deutsche Bank is another valid strategy for liquidity management by Barclays, too. Banks deploy a mix of these strategies.

The key point here is that Barclays does not need to have £100 in its vaults when it grants Eve an entitlement to £100. However, Barclays must be able to get its hands on £100 when payment in actual money is demanded, i.e. when satisfying payment demands with promises to pay does not suffice. Barclays’ ability to grant credits and collect interest on them is premised on its success in managing its income streams and financial assets.

That is, banks do not simply take possession of cash and then hand it out for a fee, but they create ability to pay. A bank cannot create ability to pay “out of thin air” but it creates it out of its and other financial institutions’ power and success in turning credit advances into financial assets and out of the thus produced creditworthiness.

The central bank asserts that credit is money.

If, at any point, Barclays can live up to the demands in hard cash against itself, i.e. if it can always pay out in money what it owes, then this works out for them. When they fail to live up to this promise this is the transition to their collapse in the form of a “bank run”: get your money out before the bank is insolvent which contributes to making the bank insolvent. Now, since banks borrow and lend to each other this, in turn, affects the ability to fulfil cash demands of other banks, triggering perhaps a bank run on them, too, etc.

Imagine the silliness of a system that builds layer after layer of credit to make the capitalist mode of production independent of something as mundane as a yellow metal and that then comes crumbling down because of a lack of this yellow metal in the right hands at the right time. Indeed, this is no longer the world we live in.

Schooled by financial crises, states placed central banks at the foundation of the systems of credit. From around 1900 most states prohibited private banks from issuing their own banknotes. Issuing banknotes, instead, became the exclusive right of the national or central bank, which sometimes formally is a private bank (but effectively under state control). In the UK, it is the Bank of England which issues the British Pound Sterling (GPB). The pieces of paper it issues, its banknotes are valid money, they are not promises of payment in money.

All private banks operating in the UK must have a bank account with the Bank of England where they must hold a fair share of their money and there were or are restrictions in place on how much credit a bank is allowed to give relative to the assets (money and “good debts” such as UK gilts) held (in the Bank of England bank account). This is a restriction of the credit operations of private banks.

On the other hand, the Bank of England creates credit without any reference to gold or any other commodity money.22 It simply decides how much money it wants to lend out according to its monetary policy. It creates this money in a similar way as private banks create money of account. They lend it out – HSBC wants a loan for £1000, the Bank of England adds £1000 to HSBC’s central bank account. The difference to private banks is that the “vault” of the Bank of England is never empty, it always has those £1000 lying around, should HSBC wish to withdraw them. They can print it and thus the BoE is always solvent. This adds a new inexhaustible and broadly-available source of credit to the liquidity management playbook of commercial banks. Therewith the banks are unfettered, their credit business is no longer based on the narrow basis of gold money or some other precious commodity but based on the credit that the Bank of England gives, i.e. fundamentally the credit that the State gives; for its macroeconomic reasons rather than the more narrow profit motives of other private banks.

So, the “resolution” to the “silliness” of building layer upon layer of credit to free the capitalist mode of production from the shackles of gold to fall back to it in every crisis is to essentially add another layer of credit, i.e. credit that is simply created by the State. How that plays out in the event of a sufficiently big crisis is a question for another text,23 here we focus on how it liberates credit from the narrow basis of precious metals or other valuable commodities.

Credit creates growth and growth anticipation creates credit

Putting these findings together, we arrive at (a) that credit creates the conditions for capitalist success and at (b) that growth anticipation creates credit. This both explains (1) the abstract possibility of inflation and that (2) the rate of inflation is a matter decided in the competition of capitals:

Inflation.

First, as explained above, in modern capitalism the purchasing power confronting the market is not limited by previously earned profits or incomes, but merely by the anticipation of future returns, by the boldness of financial capitalists in their predictions about how lucrative investments will be.

It is worth repeating: the key point here is that banks do not simply collect money from society in the form of deposits and hand out this money in the form of credit, as some sort of intermediary. Rather, banks create the ability to pay, book money, which is a promise of payment itself, and use this to grant credit. They do this to the extent that (a) they believe their debtors will pay back the loans plus interest later, (b) they anticipate they can manage their liquidity to satisfy required outgoing payments and (c) whatever constraints the law puts on them.

The limit of this sort of credit creation is not how much money in total was already earned in society (and deposited in the banks). Rather, credit is created for promising business and has its measure in anticipated success, in the boldness of capitals. The volumes of ability to pay seeking investment do not have their limit in realised sales but merely in the expected return of the business yet to be pushed into existence.

This emancipation from already realised wealth is the collective act of private banks. The volume at which they can accomplish this feat is premised on the central bank’s certification that their promises to pay are as good as its money. This equation lifts the volumes of credit that private banks can and will handle to new heights.

For the avoidance of doubt, the claim here is not that central banks cause inflation (type I) when “printing money”, i.e. lending to private banks. Rather, this inflation is a phenomenon produced by the credit operations of private banks when they create credit because they see lucrative business, i.e. in a boom. Central banks support these endeavours by providing the ultimate means of liquidity management as “lenders of last resort”. What happens when the ability of credit to start and facilitate successful business is in doubt, is another question (see below).

Rate of inflation.

Second, the relationship between credit and wealth is not simply one-sided in the sense that this speculation was right or wrong, a business succeeds or it does not. Rather, credit creates the conditions for this success, for an individual business and in the economy as a whole.

With credit, businesses can hire workers, buy materials and machines and produce more wealth, increasing the heap of commodities awaiting sale. The sale of these commodities then puts spending power of earned money into their hands to purchase from other producers who also produced on credit.

Thus, an increase in credit volumes does not directly translate to a proportional devaluation of money, in the sense of a simple quantity mismatch: more money confronting the same heap of commodities, but this increased credit volume may be the fundamental reason for an increased heap of commodities. The rate of inflation is thus explained by the motley competition of capitals for solvent demand and credit and how quickly they turn this credit into additional commodities.24

Finally, note that for credit-financed accumulation to produce a steady rate of inflation it itself needs to be steady. While a hypothetical one-off credit that is paid off, say, a year later momentarily creates additional ability to pay, this additional purchasing power is removed again when the debt is paid off. However, as mentioned above, a successful cycle – debt, business, debt has been justified – is the best reason to repeat it on a larger scale.

PS: Failed business does not explain inflation.

Some Marxist accounts of inflation, including our previous texts and seminars, conclude from the above that thus failed businesses produce inflation along the lines of: credit and thus ability to pay is created for a business but the business fails to produce more wealth, thus inflation. This is not correct. If a debtor goes bust, they are bankrupt and perhaps their creditor, too. This does not affect the money which they failed to earn.

An example. Bank Alice holds £20k worth of promissory notes. It grants capitalist Bob a loan of £10k. It adds £10k to Bob’s bank account and a demand worth £10k against Bob to its assets. It backs up this loan using its promissory notes, i.e. should Bob demand payment, the bank sells some of these notes to acquire cash to pay out Bob.

Now, Bob pays £10k to some capitalist Charley, via wire transfer between the banks Alice and Dora (Charley banks with Dora). Bank Dora now has a claim of £10k against bank Alice. Status: Bank Alice has £20k in promissory notes, a claim against Bob of £10k and there is a claim of £10k against bank Alice from bank Dora.

Finally, Bob’s business fails and he goes bankrupt. Bob cannot pay back bank Alice, so the claim of £10k against him is void. The claim of bank Dora against bank Alice remains, however. Bank Alice must sell £10k worth of promissory notes to pay out bank Dora. In summary, the end effect is that a transfer of wealth of £10k from bank Alice to bank Dora and capitalist Charley has taken place.

The initial credit produced additional ability to pay. It was produced by the anticipated success of Bob’s business not by its eventual failure. This additional ability to pay is destroyed in the end when Bob cannot pay. On the one hand, as discussed above, the additional ability to pay would also be destroyed when a debt is successfully settled without contracting new debt. However, the latter – successful – case is an encouragement to repeat the cycle whereas the former – unsuccessful – is not. Inflation requires the increased volume of ability to pay to persist and this is premised on continuous credit.

Sovereign Debt and Inflation II (A Sign of Economic Crisis)

In the last section, we discussed how financial institutions, with the support of the Central Bank and when business is good, create ability to pay that is independent of the wealth already produced and earned in society. Therewith, they unlink effective demand from produced and realised wealth. We also discussed how this ability to pay is the continuous condition for the creation of wealth in capitalist economies. They compete in this endeavour of credit creation with the capitalist state, which creates credit also and especially when business is not good.

The State maintains itself

Taxes.

The capitalist state does not earn money, it takes it – taxes are not an exchange but appropriation.25 From the taxes it levies the State organises its activities. On the one hand, it imposes its money on society when collecting taxes in it. On the other hand, it respects private interests in money when it pays its subjects for their services to itself: civil servants, suppliers and contractors.

Spending.

State spending is unproductive. While commentators and politicians like to distinguish between the “burden” of, say, benefit payments and “investments” such as HS2, except for negligible outliers state spending does not produce an increase of wealth in society (counted in money) let alone produce a return for the State. Rather, it creates conditions that allow others to invest with the prospect of a return. HS2 may be the foundation for increased business but it is not in itself increased business.26

Borrowing.

The State learned a trick or two from the capitalists it watches over. As discussed above, the rule in the capitalist economy is not to wait until profits finance an expansion but to expand on credit and to use the (anticipated) increased profits to justify the loan. The State does a similar thing: it does not wait for citizens to earn more money to receive more tax revenue which then is used for extended state activity.

Rather, the State issues bonds, in the UK these are called Gilts. More on bonds/Gilts below, for now it suffices to realise that the State borrows to finance its activity. The debts of the British State amounted to approximately £2.1 trillion in 2021.27

Economic growth can thus be promoted independently of the already existing tax income and the growing tax revenues are then used to justify the debts. On the one hand, since, as discussed above, all state spending is consumptive, state borrowing economically is like a consumer loan: the creditors do not partake in the increasing profits brought about by their credit but principal and interest are paid from income generated otherwise; here taxation (or further state borrowing, see below).

On the other hand, the State has power over society to expropriate money in the form of taxes. In this sense the State is the most solid debtor in society: it has, in principle, all of society’s wealth at its disposal. Expressed less in terms of extremes, the calculation is that with its unproductive spending the State may create the conditions for successful accumulation on its territory which in turn increases the wealth over which the State can dispose.

For businesses, borrowing is not a one-off affair, in the sense of: Borrow, spend, make money and pay back the debt. Rather, success is the best argument to pay off the old loan with new credit and then, preferably, to borrow an even higher amount. It is similar with the State: if the economy is growing this is the best argument to contract more debt to improve conditions further. Thus, sovereign debt is not of a constant size but keeps on growing. Old loans are paid off with new loans. In addition, typically more debt will be contracted (this is called “new net debt”).

Bonds.

The State borrows, as mentioned above, by issuing bonds. These are essentially like the promissory notes mentioned above. The State sells a piece of paper stating: I will pay you £50 each year for 10 years and then I will pay you £1000. This note is sold for £1000 and promises a 5% return per year for 10 years, after which the principal is paid back.

These notes – bonds – can be and are bought and sold on the “secondary market”, i.e. financial institutions trade them, for whatever price they consider profitable. If they want to get rid of their bonds from a State on whose fixed regular payments they have become less keen, they may have to sell it for less than £1000, e.g. for £833.28 To the buyer, the payment of £50 per year represents a return of 6% per year.29 This percentage is called a “yield” and thus, if the yield goes up this means bonds are bought and sold at a lower price.

The effective yield on the secondary market in turn informs what yield the State must offer when issuing new bonds. So if its previously issued “I pay you £50 per year” bonds trade at a price producing a yield of 6%, then new £1000 bonds issued and sold by the State must promise £60 to find purchasers.

Given that these bonds are issued by the most reliable debtor in society, they are considered rather safe investments. In addition, the volume of these bonds is massive and so is the trade in them. This means they can be turned into hard cash on the secondary market on relatively short notice and at relatively predictable prices. Thus, as alluded to above, instead of hoarding cash for liquidity management, banks may and do hoard these bonds, they are essentially as safe as cash but also earn interest. So the debt issued by the State is treated almost like cash itself. In this way, the sovereign debt issued by capitalist states is itself a fundamental contribution to the foundation of the credit business of private banks.

Sovereign debt and inflation I.

Despite its different economic determinations, when business is good, the State’s debt functions not that differently from that of private businesses. The State borrows money and uses this to purchase commodities, either directly or by paying wages which are then turned into groceries and so on. Additional credit-backed purchasing power thus confronts the world of commodities. Now, while all state spending is unproductive, its activities may still create, maintain and promote the foundation for successful private business, which in turn produces additional wealth. Thus, here too a simple formula – this much additional sovereign debt leads to that much inflation – cannot be obtained, it depends on what private businesses do with the conditions produced by the State.

Logic.

However, the State’s credit operations differ not only in volume from those of private banks but also in rationale. When business is down the State takes on credit and spends this borrowed money. In a recession, tax revenue is reduced as fewer commodities are sold, lower or fewer profits are realised and fewer people are in jobs. At the same time, the need for state activity increases to maintain society, e.g. those unemployed people or key branches of industry. All of this is financed by credit.

Furthermore, through “counter-cyclical fiscal policy” the State may go beyond maintaining its society and may try to stimulate the economy to get out of the current slump. If this works is out of scope for this piece. Here, we only remark that this, too, is financed by credit.

Where private banks dry up the credit supply and demand when the business of their debtors does not look too good, the State increases the volumes of debt contracted in a downturn. Of course, private banks, too, have to decide on whether to follow one credit with another to get a debtor through a slump. But this then puts a strain on their liquidity management and if the slump persists they will pull the plug. The bank writes off the loan or, if it has misjudged its liquidity management, goes bankrupt itself. Either way, it does not indefinitely continue to borrow money to credit its debtors. The State, in contrast, successfully continues to borrow to maintain itself and its society.

The State can do this, i.e. its credit remains in demand, because of the tight identification of sovereign debt and money. Both on the secondary market and with the Central Bank, sovereign bonds can be exchanged for actual money or used as collateral when borrowing money.30 Holding on to the sovereign debt issued by the State is like holding on to the money of its Central Bank.

Second, the State cannot go bankrupt, for its debt to be written off.31 Its attempts at reviving the economy may be unsuccessful and growth may not follow, but this does not invalidate the outstanding claims against it. Sure, their price on the secondary market may suffer, but the State does not become insolvent. Its credit remains and is not wiped out.

The State’s credit operations in times of a downturn – to replace and to stimulate economic activities – are the transition to a second form of inflation.

Crisis intervention by the State

In a crisis, financial institutions cancel themselves by cancelling their mutual trust in their assets. Having lived off the assertion that debt is an asset, almost as good as payment, their mutual construction comes crashing down when they doubt this assertion. In such a crisis, the economy grinds to a halt, investments are not worthwhile, purchases do not take place and thus no sales, either.

The result of this crash is not inflation, but a nationwide collapse of business combined with the danger of a collapse of the social circulation of money. Little is bought or sold. The national business perishes as a result, not the national money. If anything, investors try to offload their wobbly debt instruments to get their hands on cash, i.e. central bank money.

In this situation, the State considers it necessary not only to return to growth but to somehow avoid the outright collapse of already booked growth, debt counted as wealth, and thus to prevent losses for and collapses of financial capitals and ultimately its entire national economy.32

Central Bank.

(1) The Central Bank reduces “the price of money”, i.e. the interest rate it charges financial institutions to borrow from the Central Bank. This is meant to prevent panic sell-offs to gather cash to pay off liabilities.

(2) The Central Bank continues to accept debt obligations that are now foul as collateral when borrowing cash from it or outright buys these papers, an operation known as “quantitative easing”. This prevents the collapse of these debt instruments and thus their (now former) holders. It may even reconstitute trust in these promises to pay so that they function again as assets. Indeed, this might lead to investment in these assets again.

These two measures – and these involve massive sums – do not have an inflationary effect during a crisis. The money the Central Bank mobilises for these operations does not immediately end up in the hands of capitalists to purchase commodities. As such, this does not immediately contribute to inflation. This could be empirically observed since 2013 when central banks mobilised vast sums for their quantitative easing programmes without this producing a significant inflationary effect.

However, these operations keep promises to pay in value which do not correspond to successful accumulation. Thus, in contrast to the example of a failed business mentioned above the increased ability to pay is not wiped out. As such, when business prospects improve after the crisis this may encourage bolder credit-granting decisions, i.e. when these assets back credit to businesses who then invest, but it does not do so during the crisis.

State.

(3) The other big crisis measure of the State are stimulus programmes or, in the extreme, keeping itself afloat. The State issues bonds – debt that is essentially equivalent to the money the Central Bank prints, an equation the Central Bank actively supports when it buys bonds issued by its own State – to finance its activities and to stimulate the economy. The State pays wages and buys goods and services. The key point here is that the State effectively prints money and spends it.

Faced with the failure to realise its ambition to maintain itself through the money it issues, the State insists on it against the economic reality. It insists on the validity and power of its money by pushing more into society. Money does not command social wealth, little can be bought for it, so the State mobilises more money to overcome this lack of purchasing power. This money, however, does not meet a capitalist economy where this money is the central means of enrichment, but an economy in crisis. Thus, the Bank of England has it the wrong way around when it writes:

“In extreme cases, high and volatile inflation can cause an economy to collapse. Zimbabwe is a good example. It experienced this in 2007-2009 when the price level increased by around 80 billion per cent in a single month. As a result, people simply refused to use Zimbabwean banknotes and the economy ground to a halt.” (Bank of England. What is inflation? 3 Feb 2022.)

The State’s excessive printing of money is a response to its economy collapsing not its cause. Runaway inflation is a phenomenon of a crashed economy and a State that insists its money still functions in commanding social wealth.

Summary

In summary, “inflation” refers to quite disparate economic phenomena: 5% or so corresponds to an economic boom and does not threaten the capitalist economy at all, it is rather a phenomenon of its success. In contrast, 200% or so of “hyperinflation” where money rapidly loses its value in days corresponds to a collapsing economy. These are qualitatively different situations, not just different quantities. The former is produced by financial institutions with the support of the Central Bank, the latter is produced by the State refusing to concede that its central means of rule – its money – fails to command a society where the economy is down.

Press

“Labour shortages”

“But the MPC [Monetary Policy Committee] warned that if labour shortages proved bigger and more persistent than expected — if workers were in the wrong place, or had the wrong skills, for the jobs available, or if young people who had left the labour market to study stayed in education for some years — that was likely to make wages rise, inflation more persistent and the BoE raise interest rates.

When it does become time to tighten monetary policy, the BoE also changed its guidance on Thursday on how it will make borrowing more expensive for households, businesses and government.” – Chris Giles and Delphine Strauss. BoE sees tight labour market as trigger for higher rates in Financial Times. 5 August 2021

Growth

“Britain’s economy surged forward in the second quarter, growing 4.8 per cent as consumers eagerly spent money following the easing of coronavirus restrictions and the progress of the country’s vaccination programme.

The rapid quarter-on-quarter growth rate allowed the economy to recover much of the ground lost over the past two years. Still, it produced 4.4 per cent fewer goods and services between April and June than in the final quarter of 2019.

The growth rate was in line with market expectations, although a touch slower than the Bank of England’s forecast of 5 per cent expansion.

With the US having recovered all of its lost ground in the second quarter and eurozone output 3 per cent below the pre-pandemic peak in the same period, the figures showed the UK’s economic performance was still lagging behind other advanced economies.” – Chris Giles. UK economy grows 4.8% in second quarter in Financial Times. 12 August 2021

“The eurozone economy has bounced back from its historic pandemic-driven downturn, logging faster than expected growth of 2 per cent in the three months to June, according to data released on Friday.

The quarter-on-quarter rise in eurozone gross domestic product was higher than the 1.5 per cent expected by economists polled by Reuters and is the first time the bloc has outpaced growth in the US and China since the pandemic started last year. It also marked a strong rebound from the bloc’s 0.3 per cent contraction in the first quarter.” – Martin Arnold. Growth returns to eurozone with healthy rebound in second quarter in Financial Times. 30 July 2021

“Persistence of demand for goods”

“The inflationary surge has taken many economists by surprise. In some countries — such as the US, Canada, the eurozone, Brazil and Peru — inflation forecasts for this year have doubled in only a few months, according to Consensus Economics, a company that tracks leading forecasters.

‘Economists have been caught out by a few things — energy prices, which are famously hard to forecast, and the persistence of demand for goods even as economies have reopened,’ said James Pomeroy, global economist at HSBC.” – Valentina Romei. The unexpected surge in inflation, in charts in Financial Times. 21 November 2021

“Strong demand for most goods and services”

“Economists polled by Reuters forecast inflation to hit 5.2 per cent, the joint highest since the early 1990s and up from a decade-high of 5.1 per cent in November. They attribute the upward price pressure to higher energy costs, strong demand for most goods and services, and continued supply chain disruption.” – Valentina Romei. UK inflation set to hit 30-year high as rate rise expectations mount in Financial Times. 18 January 2022

“Wage-price spiral”

“It is being closely watched by policymakers at the Bank of England, who are acutely worried that a surge in inflation — initially caused by higher global prices for goods and energy — could become a lasting phenomenon if it gets baked into domestic wage settlements.

Most forecasters expect the monetary policy committee to raise interest rates when it meets on Thursday, to avert the risk of a so-called wage-price spiral developing, when workers demand pay rises to match higher living costs and companies raise prices to protect their margins in a repeating, self-fulfilling process.” – Delphine Strauss. Can the UK avoid a wage-price spiral? in Financial Times. 1 February 2022

“Clothing and footwear”

“Grant Fitzner, ONS chief economist, said that ‘clothing and footwear pushed inflation up this month’ together with the rising costs of some household goods.” – Valentina Romei. UK inflation climbs to 30-year high of 5.5% in Financial Times. 16 February 2022

“Ukraine conflict”

“Inflation has hit its highest level in decades for many countries, with the Ukraine conflict adding upward pressure on energy prices and squeezing households’ real incomes.

Russia’s invasion of its neighbour has pushed up energy and food prices at a time when many countries were already registering near-record rates of consumer price growth, leading some economists to fear a general return to the chronic inflation of the 1970s. High inflation is geographically broad-based even if East Asia has largely been an exception to the worldwide pattern.” – Valentina Romei and Alan Smith. Inflation tracker: latest figures as countries grapple with rising prices in Financial Times. 18 March 2022

Footnotes

1 It is the fetishism of commodities par excellence: “The mysterious character of the commodity-form consists therefore simply in the fact that the commodity reflects the social characteristics of men’s own labour as objective characteristics of the products of labour themselves, as the socio-natural properties of these things. Hence it also reflects the social relation of the producers to the sum total of labour as a social relation between objects, a relation which exists apart from and outside the producers.” (Karl Marx. Capital, Vol. 1. p.164)

2 “Is high inflation a problem? A healthy economy needs to have a low and stable rate of inflation. The Government sets a target for how much prices overall should go up each year in the UK. That target is 2%. It’s the Bank of England job to keep inflation at that target. A little bit of inflation is helpful. But high and unstable rates of inflation can be harmful. If prices are unpredictable, it is difficult for people to plan how much they can spend, save or invest.” (Bank of England. What is inflation? 3 Feb 2022.)

3 A refreshingly honest take is given in the biggest conservative German newspaper: “Companies make a big mistake when they raise their prices too late in inflation. Some suppliers delay price increases because they hope to gain market share. But that goes wrong. My advice to companies is therefore: raise prices faster! Price increases should not be below the inflation rate, but rather slightly above it. That also works easier in an inflation.” (Hermann Simon in „Erhöht die Preise schneller!“ in Frankfurter Allgmemeine Zeitung. 26 Mar 2022)

4 “Even before Russia’s invasion of Ukraine, consumer prices were pushed upwards by global factors, particularly the economic recovery from the worst of the pandemic and supply constraints in certain sectors.” (Andrew Bailey, Governor of the Bank of England. Letter from the Governor to the Chancellor. 17 Mar 2022)

5 The Bank has one set of answers to the question “where does inflation come from” that it gives in its Governor’s letters to the Chancellor. We discussed those above. In its monetary policy, the Bank presumes a different explanation, which we discuss here.

6 “Only because the farmer has sold his wheat is the weaver able to sell his linen, only because the weaver has sold his linen is our rash and intemperate friend able to sell his Bible, and only because the latter already has the water of everlasting life is the distiller able to sell his eau-de-vie. And so it goes on.” (Karl Marx. Capital, Vol. 1. p.207)

7 If anything, in response to inflation many people borrow to bridge the gap between their wages and their costs, often at interest rates significantly higher than what the BoE sets due to the risky nature of these consumer loans. See e.g. Leke Oso Alabi and Siddharth Venkataramakrishnan. Pawnbroking surges in UK amid cost of living squeeze in Financial Times. 29 Jul 2022 or Oliver Ralph. UK consumer borrowing doubles amid rise in cost of living in Financial Times. 29 Jul 2022. See also a footnote below.

8 It should also talk about the State, see below, but seemingly it does not.

9 The Bank explains this in e.g. Michael McLeay, Amar Radia and Ryland Thomas. Bulletin 2014 Q1: Money creation in the modern economy. 2014

10 See “Central Bank Policy since 2013” in Economic Crisis (from 2007 to June 2020).

11 The discussion so far also gives a hint as to why the Bank of England is so worried about wages. It knows of the relationship between wages and profits we based our argument on above: higher wages reduce profits. It also knows that the profitability of businesses, their ability to turn (credit-backed) advances into surpluses, is what everything from the value of the money the Bank of England issues to the livelihood of everybody in society depends on.

12 “This part of the value of the commodity, which replaces the price of the means of production consumed and the labour-power employed, simply replaces what the commodity cost the capitalist himself and is therefore the cost price of the commodity, as far as he is concerned. (…) On the other hand, however, the cost price of the commodity is by no means simply a category that exists only in capitalist book-keeping. The independence that this portion of value acquires makes itself constantly felt in practice in the actual production of the commodity, as it must constantly be transformed back again into the form of productive capital by way of the circulation process, i.e. the cost price of the commodity must continuously buy back the elements of production consumed in its production.” (Karl Marx. Capital, Vol. 3, p.118)

13 Inflation-adjusted earnings are a thing. This means, on the one hand, that capitalists know that their unit is not a unit, that what they presuppose as fixed is not fixed. This also means, on the other hand, that they seek a fixed standard, a unit, by which to judge their success. Their business is premised on it.

14 “On the basis of capitalist production, money – taken here as the independent expression of a sum of value, whether this actually exists in money or in commodities – can be transformed into capital, and through this transformation it is turned from a given, fixed value into a self-valorizing value capable of increasing itself. It produces profit, i.e. it enables the capitalist to extract and appropriate for himself a certain quantity of unpaid labour, surplus product and surplus-value. In this way the money receives, besides the use-value which it possesses as money, an additional use-value, namely the ability to function as capital. Its use-value here consists precisely in the profit that it produces when transformed into capital. In this capacity of potential capital, as a means to the production of profit, it becomes a commodity, but a commodity of a special kind. Or what comes to the same thing, capital becomes a commodity.” (Karl Marx. Capital, Vol. 3, p.459)

15 This qualitative difference in the economic substance of the debt relation finds expression in the quantitative difference of interest rates. Payday lenders charge about 1,250% annual percentage rate (APR), credit cards about 20%, personal loans about 8%. The BoE interest rate in August 2022 was 1.75% per year.

16 The SPGB and others would object to this statement. For example, they write: “Basically, they (banks) are financial intermediaries, accepting money originally generated in production from business and individuals who don’t want to spend it immediately (but to ‘save’ and spend later) and lending most of this to fund some business project or purchase.” (The Magic Money Myth)

17 “In the direct form of commodity circulation hitherto considered, we found a given value always presented to us in a double shape, as a commodity at one pole, and money at the opposite pole. The owners of commodities therefore came into contact as the representatives of equivalents which were already available to each of them. But with the development of circulation, conditions arise under which the alienation of the commodity becomes separated by an interval of time from the realization of its price. (…) The seller sells an existing commodity, the buyer buys as the mere representative of money, or rather as the representative of future money. The seller becomes a creditor, the buyer becomes a debtor.” (Karl Marx. Capital, Vol. 1, p.232) “I have already shown (in Volume 1, Chapter 3, 3, b) how the function of money as means of payment develops out of simple commodity circulation, so that a relationship of creditor and debtor is formed. With the development of trade and the capitalist mode of production, which produces only for circulation, this spontaneous basis for the credit system is expanded, generalized and elaborated. By and large, money now functions only as means of payment, i.e. commodities are not sold for money, but for a written promise to pay at a certain date. For the sake of brevity, we can refer to all these promises to pay as bills of exchange.” (Karl Marx. Capital, Vol. 3, p.525)

18 Promissory notes have now largely been replaced by services of banks and thus are not common anymore. The historical example here is meant to help to explain the logical development step by step.

19 “Credit-money springs directly out of the function of money as a means of payment, in that certificates of debts owing for already purchased commodities themselves circulate for the purpose of transferring those debts to others.” (Karl Marx. Capital, Vol. 1, p.238) “Until they expire and are due for payment, these bills themselves circulate as means of payment; and they form the actual commercial money.” (Karl Marx. Capital, Vol. 3, p.525)

20 “With the concentration of payments in one place, special institutions and methods of liquidation develop spontaneously. For instance, the virements in medieval Lyons. The debts due to A from B, to B from C, to C from A, and so on, have only to be brought face to face in order to cancel each other out, to a certain extent, as positive and negative amounts. There remains only a single debit balance to be settled. The greater the concentration of the payments, the less is this balance in relation to the total amount, hence the less is the mass of the means of payment in circulation” (Karl Marx. Capital, Vol. 1, p.235) “To the extent that they ultimately cancel each other out, by the balancing of debts and claims, they function absolutely as money, even though there is no final transformation into money proper.” (Karl Marx. Capital, Vol. 3, p.525)

21 “As these mutual advances by producers and merchants form the real basis of credit, so their instrument of circulation, the bill of exchange, forms the basis of credit money proper, banknotes, etc. These are not based on monetary circulation, that of metallic or government paper money, but rather on the circulation of bills of exchange.” (Karl Marx. Capital, Vol. 3, p.525) Here, “government paper money” refers to money that is, at least notionally, tied to a money commodity. It does not exist any longer.

22 “Since the Bank of England’s (the ‘Bank’) foundation in 1694 the Bank has issued notes promising to pay the bearer a sum of money. For much of its history the promise could be made good by the Bank paying out gold in exchange for its notes. (…) The link with gold was finally broken in 1931 and since that time there has been no other asset into which holders have the right to convert Bank of England notes. They can only be exchanged for other Bank of England notes.” (Bank of England, What is the value of the sterling currency? 25 Feb 2016)

23 See “The Global Economy in Early 2020 – A Conclusion” in Economic Crisis (from 2007 to June 2020) for some discussion on this.

24 It also depends on whether this credit is used by the debtors to buy commodities or, say, financial assets like shares or bonds.

25 See “I pay my taxes” – so what?!

26 Of course, for the contractors working on HS2, this is a profitable business. But just like your spending on cornflakes is consumptive and not productive despite being a profit-laden business for the seller, this does not alter the fact that the State’s spending is consumptive.

27 For comparison, all “non-financial corporations, households and non-profit institutions serving households” combined held £3.5 trillion on debt in 2019.

28 Since dividends paid on bonds are fixed, example reasons to become less keen on those are that other investments promise higher returns or that inflation eats too much into the gains.

29 This is a simplification. The maths does not quite work out neatly to 50/833 = 6% because the bond purchased on the secondary market for £833 promises £50 per year and the eventual payment of £1000, which represents an additional profit of £1000-833 = £167. This is taken into account.

30 “The central bank’s share of UK bonds pushed above 30 per cent at the most recent reading by the DMO, released at the end of last month and covering up to the end of September 2020.” (Joshua Oliver. Bank of England tops private investors as biggest holder of gilts in Financial Times. 12 April 2021)

31 Sovereign default exists internationally, i.e. in foreign money, but not internally. The State is always solvent in its own money, but this money can collapse. This is what we are discussing here.

32 The State also supports its wider economy by reducing wages and non-wage costs, either directly or indirectly by reducing benefits – which represent a de facto floor for wages, cf. The Dubious Benefits of a Workers’ State: Universal Credit. Suppressing wages does not add inflationary pressure, but we mention it here for completeness.